Amortisation

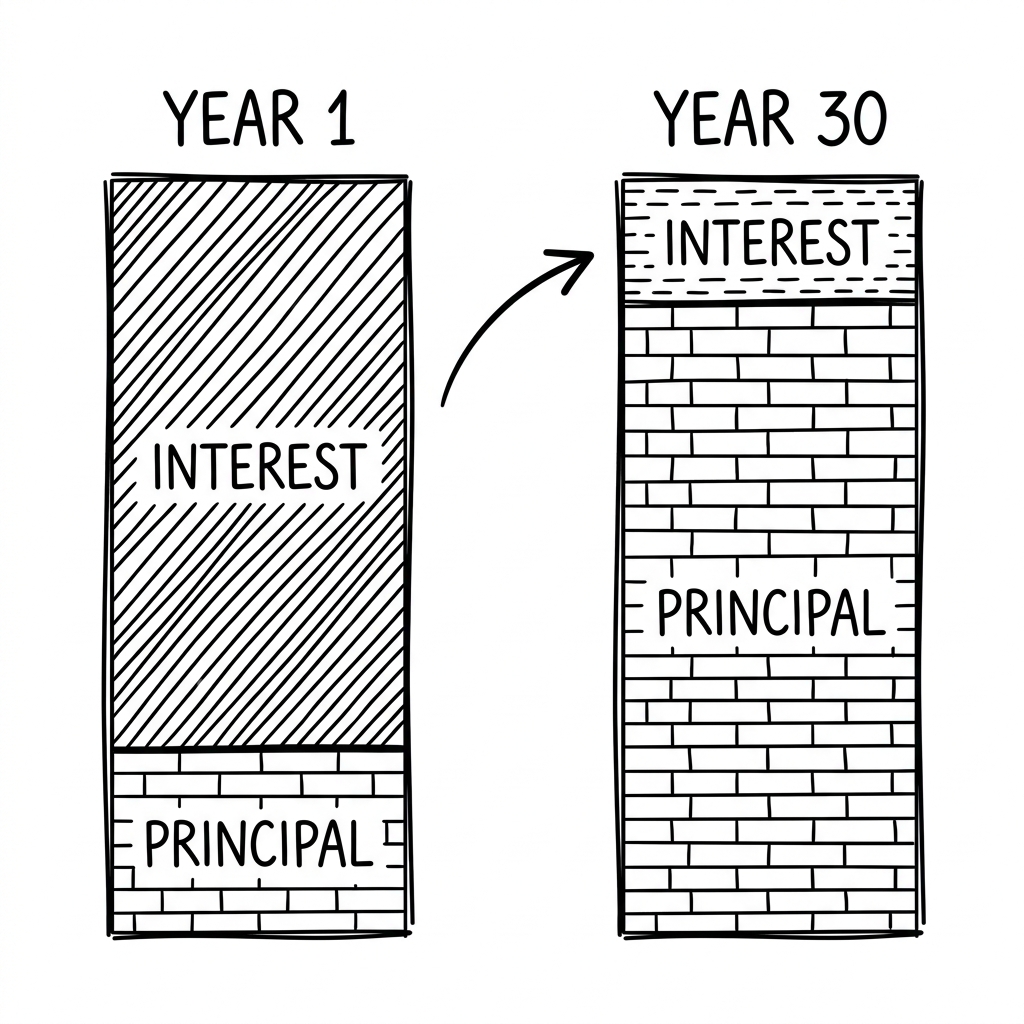

Amortisation is the structured process of repaying your mortgage over time through regular payments. Each payment you make is split into two parts: a portion that reduces the principal (the amount you originally borrowed) and a portion that covers the interest charged on the outstanding balance. The total payment amount stays the same each month, but the ratio between principal and interest shifts significantly over the life of the loan.

In the early years of a mortgage, the bulk of each payment goes toward interest, because the outstanding balance is at its highest. As you continue making payments and the principal shrinks, less interest is charged each month, meaning a progressively larger slice of each payment chips away at what you owe. By the final years of a 30-year mortgage, the vast majority of each payment is reducing the principal.

This is why making additional repayments early in a mortgage can have a disproportionate impact on the total interest you pay. Every extra dollar applied to the principal reduces the balance the bank uses to calculate your interest, compounding the benefit over the remaining term.

Understanding amortisation helps you see why the true cost of a mortgage is significantly higher than the amount borrowed. The longer the loan term, the more total interest you pay, even if the monthly repayment is more manageable. Shortening your loan term or making extra repayments where possible can substantially reduce the total cost of the loan.

Related Terms

See how this affects your numbers

Run the mortgage calculator to see how amortisation plays out in your specific situation.